Tracking Key Economic Indicator Trends

September 2024 Quarter compared to the June 2024 Quarter

The September 2024 consensus forecasts reflect a cautious economic outlook, with marginal upward adjustments in inflation and interest rates offset by weaker growth expectations. The RBA’s tighter monetary policy stance suggests a continued focus on controlling inflation, even at the expense of slower growth. Businesses should prepare for a challenging short-term environment while remaining optimistic about medium-term stabilisation and recovery.

Each of the graphs below illustrates how consensus economic forecasts evolve over each quarter. These visual representations depict whether the consensus expectation has increased or decreased when compared to the previous quarter.

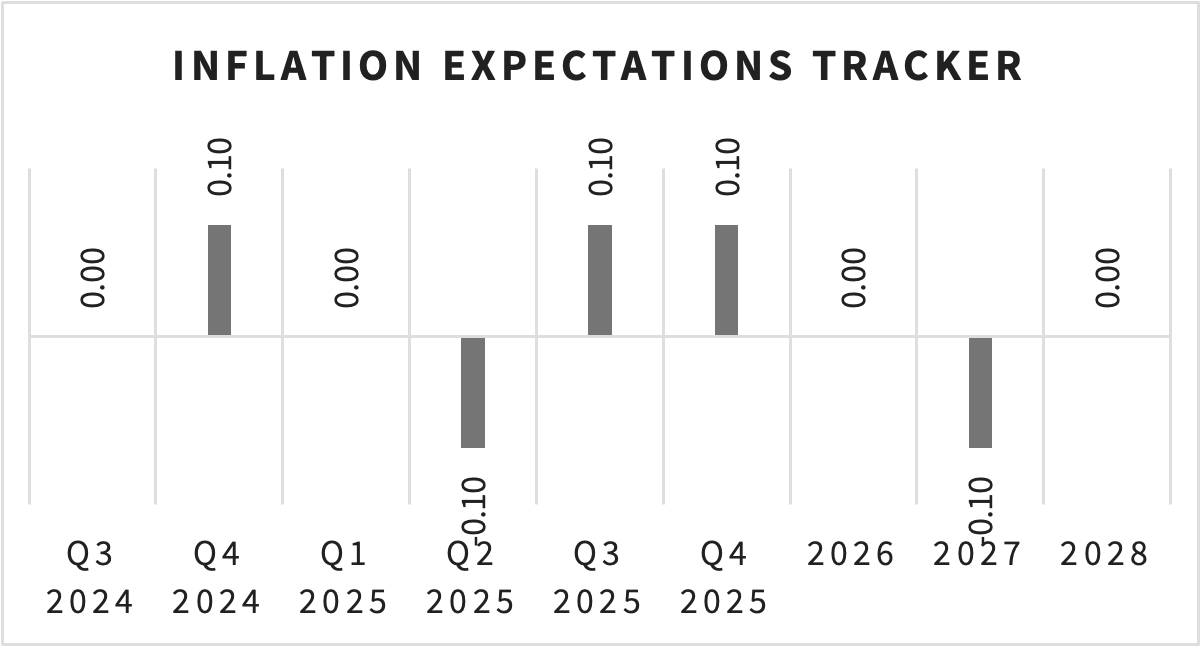

Inflation (CPI)

Short-Term Adjustments (2024–2025):

Consensus inflation projections remain largely unchanged for Q3 2024 (0.00%), with a +0.10% revision for Q4 2024.

A slight downward adjustment of −0.10% is expected in Q2 2025, followed by a +0.10% revision for Q3 and Q4 2025.

Medium-Term Stability (2026–2028):

Consensus inflation forecasts for 2026 and 2028 remain unchanged, while 2027 sees a slight downward revision of −0.10%. These adjustments suggest continued alignment with the RBA’s target range of 2–3%.

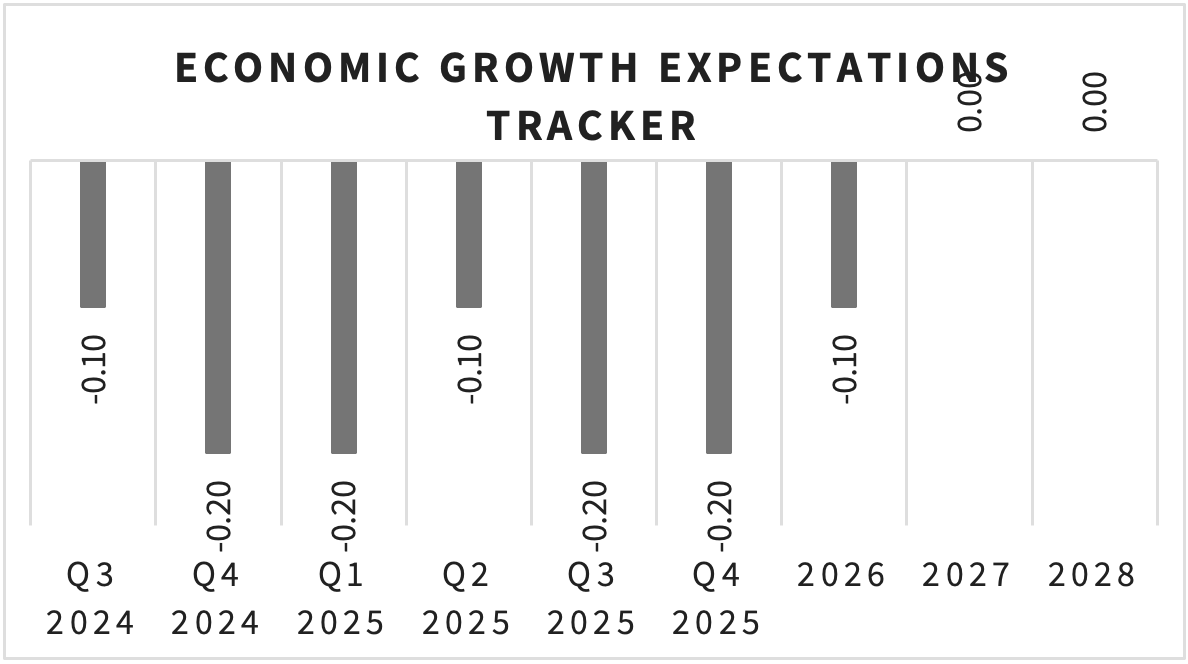

Economic Growth (GDP)

Short-Term Revisions (2024–2025):

Consensus economic growth forecasts have been revised downward, with Q3 2024 (−0.10%) and Q4 2024 (−0.20%) reflecting a weaker-than-expected recovery.

Similar downward revisions of −0.20% are evident for Q1, Q3, and Q4 2025, with Q2 2025 seeing a smaller adjustment of −0.10%.

Medium-Term Stability (2026–2028):

Consensus growth forecasts for 2026 and 2027 reflect slight downward adjustments of −0.10% and 0.00%, respectively. Projections for 2028 remain unchanged, suggesting stabilisation in the medium term.

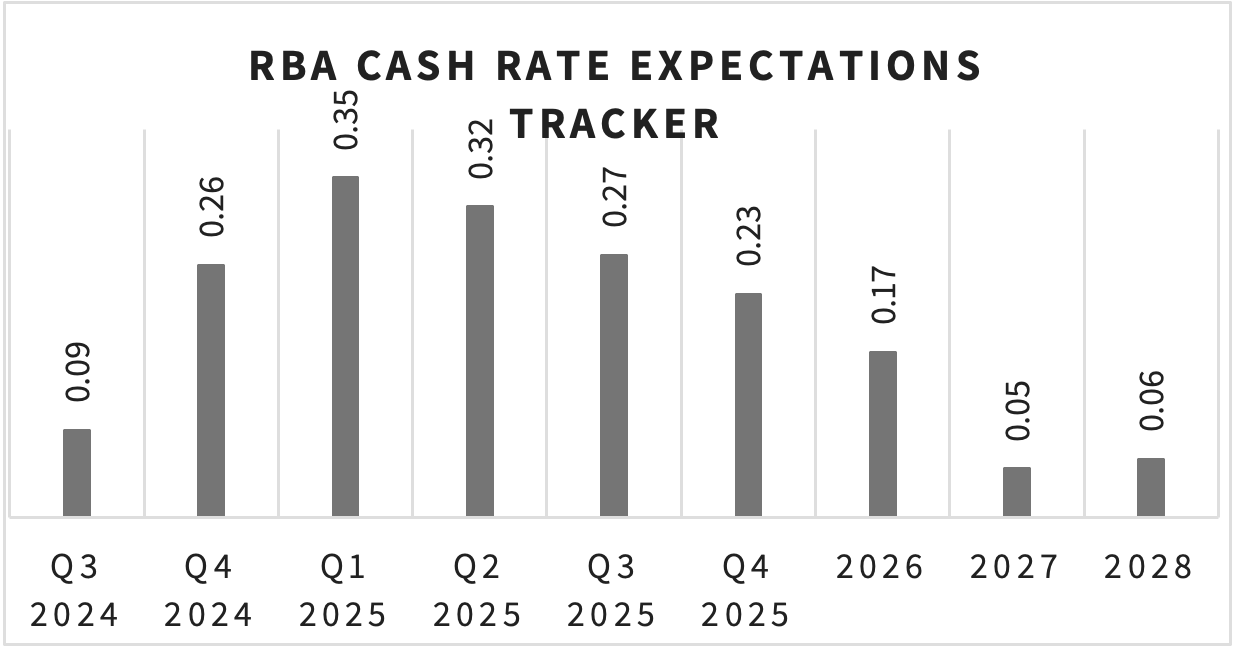

RBA Cash Rate

Short-Term Adjustments (2024–2025):

The RBA cash rate has been revised upward across all quarters in 2024 and 2025, indicating tighter monetary policy. These adjustments reflect the RBA’s response to persistent inflationary pressures and the need to maintain price stability.

Medium-Term Projections (2026–2028):

The cash rate is expected to decline gradually, with minor upward revisions of +0.17% in 2026 and +0.06% in 2028. These adjustments suggest a slower pace of monetary easing than previously anticipated.

Disclaimer

This document is provided for informational purposes only and does not constitute professional advice. The economic forecasts and analyses presented are based on consensus data from FocusEconomics. These projections are subject to change and uncertainty.

The information contained herein has been obtained from sources believed to be reliable, but Market Line makes no representations or warranties as to its accuracy, completeness, or suitability for any particular purpose. Any reliance you place on such information is strictly at your own risk.

The economic projections and opinions expressed in this newsletter are general in nature and do not take into account the specific circumstances, financial situation, or particular needs of any individual or entity. They should not be construed as recommendations to make any investment decisions or to take any specific actions.

Market Line and its employees shall not be liable for any loss or damage, direct or indirect, arising from the use of or reliance upon any information contained in this newsletter.

© 2024 Market Line Pty Ltd (ACN 644 883 483) is Corporate Authorised Representative Number 1284459 of AFSL 3442034